Sometimes, headlines can be deceiving. The consensus sees a number like 7.4% GDP growth and assumes everything is booming. Or they see low inflation and assume demand is dead. Both are wrong. As a macro-strategy analyst, we have to look past the scary stories and the cheerleading to see what the market actually cares about: The Gap Between Expectation and Reality.

In this Q&A, I have tried to break down the First Advance Estimates (FAE) numbers, but ignores the noise to focus on what they actually mean for the cycle, the strategy, and your portfolio.

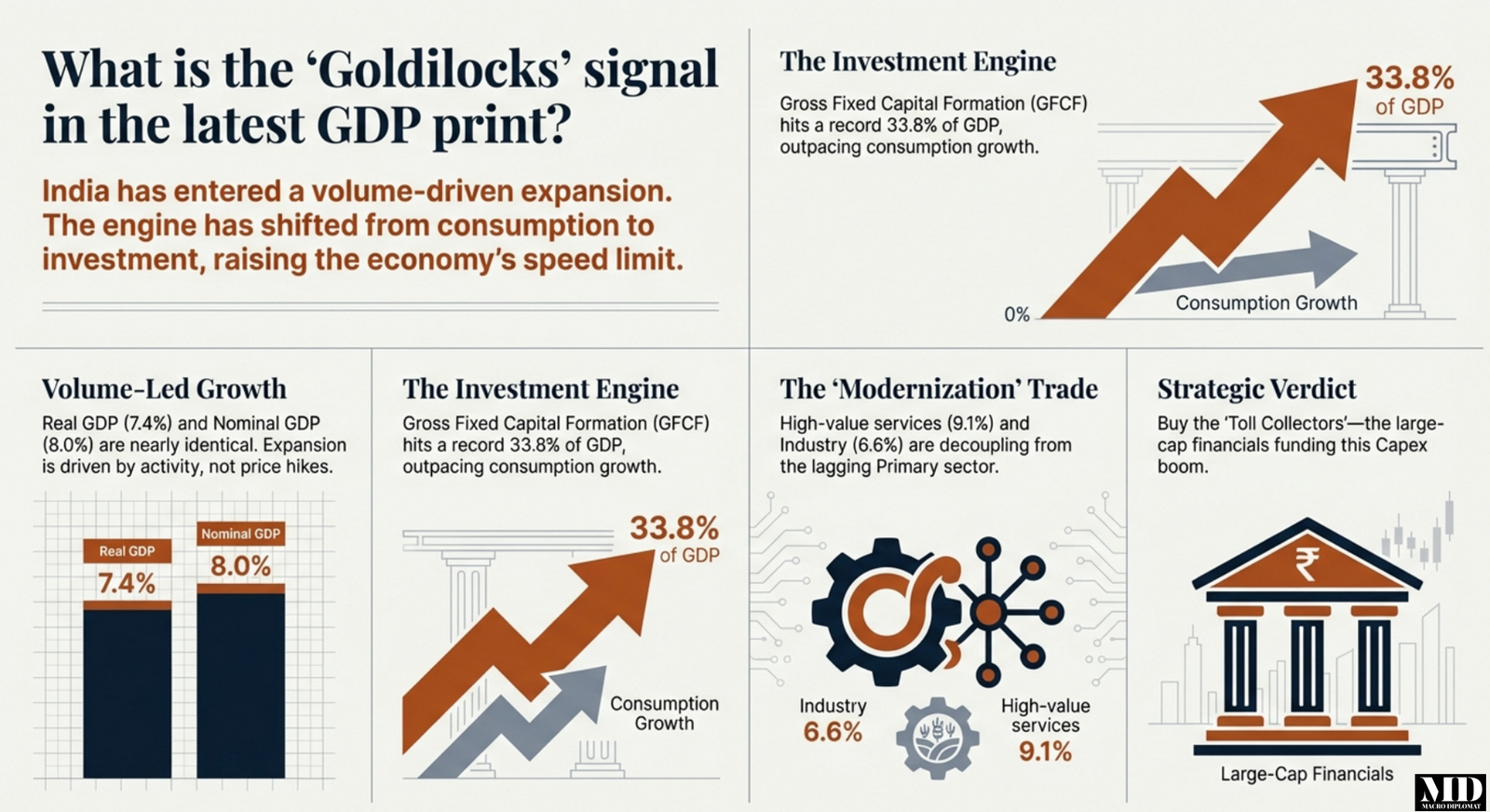

1. What does 7.4% GDP growth actually tell us about where India is in the cycle?

Data recap:

- Real GDP growth: 7.4% (vs 6.5% last year).

- Real GVA growth: 7.3%.

- Nominal GDP growth: 8.0% (vs 9.8% last year).

- Implied GDP deflator: ~0.6%.

I think this is a statistical anomaly that screams “Opportunity.” Look at that spread between Real (7.4%) and Nominal (8.0%). It is razor-thin. This is highly unusual for an Emerging Market. Usually, when EMs boom, they inflate. They pump up the numbers with price hikes.

India is doing the opposite. This isn’t a fragile, inflation-fueled upturn; it is a Volume-Driven Expansion.

We are clearly past the “Recovery” phase and deep into “Expansion.” But here is the kicker: we aren’t overheating. If we were overheating, that deflator would be 5% or 6%. At 0.6%, it tells you the constraint today isn’t capacity—it’s pricing power.

The Corporate Reality: Firms are selling massive volumes (hence the 7.4% real growth), but they can’t raise prices (hence the low deflator). Margins are under pressure from competition, but activity is sky-high.

The Policy Signal: For the RBI, this is the ultimate “Goldilocks” scenario. The data is screaming, “Inflation is dead for now; go for growth.” For the Finance Ministry, it’s trickier—they hit their deficit targets because the denominator (GDP) is big, but the actual tax collections (Nominal) are softer than they’d like.

So the net takeaway is that the economy is growing fast, but in a world of cheap prices. That is a “high-quality” growth story, even if it feels tough for corporate pricing managers.

2. Is this really an investment‑led cycle—or still a consumption story in disguise?

Data recap (constant prices):

- PFCE (Consumption) growth: 7.0%; Share: 56.3% (flat).

- GFCF (Investment) growth: 7.8%; Share: 33.8% (record high).

- GFCE (Govt Spending) growth: 5.2%.

The “India is a consumption story” narrative is yesterday’s news. The data shows consumption is now just the base—it’s steady, it’s fine, but it’s not the engine.

The engine is Investment (Capex).

The Shift: Look at that Investment ratio: 33.8% of GDP. That is the highest in the current series. When investment grows faster than consumption, markets cheer. Why? Because consumption is for today, but investment builds earnings for tomorrow. This composition—roads, logistics, factories, digital infra—is exactly what raises a country’s Potential GDP. It means supply will keep up with demand, keeping future inflation down.

The “Crowding In”: This isn’t just the government digging holes and filling them up. A 7.8% jump in GFCF signals that private capex is joining the public infrastructure party.

The character of this growth has changed. It is “Capex-Led, Services-Supported.” Consumption is just the passenger, not the driver.

3. What do the sectoral numbers say about India’s structural direction?

Data recap (real GVA growth):

- Tertiary (Services): 9.1% (Finance, Real Estate, Public Services leading).

- Secondary (Industry): 6.6% (Manufacturing & Construction both at 7.0%).

- Primary (Ag & Mining): 2.7% (Agriculture 3.1%, Mining -0.7%).

I believe, this is the “Modernization” trade playing out in real-time.

Services growing at 9.1% confirms India is structurally moving toward knowledge and capital-intensive work. Finance and Real Estate aren’t just paper-pushing; they are the grease for the capex engine we just talked about.

Industry is Real: For years, “Make in India” was just a slogan. Now, with Manufacturing and Construction both hitting 7.0% (though smaller than services but coming from a higher base), it’s a reality. We are seeing actual output, not just MOUs.

The Decoupling: Here is the harsh truth—the Primary sector (Agriculture/Mining) is divorcing the rest of the economy. When the farm grows at 3% and the city grows at 9%, you get a massive income divide.

Strategic Implication: The “High-Value Services + Industrial Capex” model is great for aggregate GDP and stock market earnings (since listed companies are mostly in these sectors). But socially? It forces a choice: either labor migrates out of farming fast, or you get a persistent rural underclass.

4. How should we interpret the agriculture shock: 3.1% real but only 0.8% nominal?

Data recap (agriculture & allied):

- Real GVA: +3.1% (Volume is up).

- Nominal GVA: +0.8% (Income is flat).

- Implied deflator: ~−2.3% (Deflation).

This is a classic “Terms of Trade” squeeze, and it explains why the “vibes” in the countryside are terrible even though the GDP is 7.4%.

The Deflation Tax: A decade ago, urban India paid an “inflation tax” (high prices). Now, rural India is paying a “deflation tax.” Farmers are producing more volume (record harvests) but getting paid less for it.

The Consumption Impact: Farmers spend in Rupees, not in “Real GDP percentages.” When their nominal income grows at 0.8%, they stop buying motorcycles, tractors, and FMCG goods. This is why you hear “rural slowdown” on every earnings call.

The Political Risk: Markets hate uncertainty. An economy where the city booms and the village busts invites government meddling—loan waivers, higher support prices (MSPs), or handouts.

Stop watching the harvest; watch the wallet. Agriculture isn’t facing a Growth Crisis—we have plenty of rice and wheat. It is facing an Income Crisis. This is a political problem masquerading as an economic one. For the upcoming budget, the Finance Minister needs to stop obsessing over MSP (Minimum Support Price). MSP is just a floor; it’s a safety net, not a ladder. The real game changer isn’t paying farmers more to grow the same low-margin grains; it is helping them capture the value of what they grow. The pivot we need? Price Realization, not just Price Support. That means pushing hard into high-value crops, creating non-farm jobs to absorb excess labor, and aggressively funding the Food Processing sector. The goal shouldn’t be just growing tomatoes; it should be turning them into ketchup before they rot. That is how you fix the rural income statement.

5. What does the investment ratio of 33.8% really signal about medium‑term growth?

Data recap:

- Investment (GFCF) share in GDP: 33.8%, up from 33.7% and 33.5%.

This is the single most bullish number in the print. We have had three years of investment ratios in the mid-30s. This isn’t a blip; it’s a structural shift. The “baseline” for investment has moved up.

- Raising the Speed Limit: Consensus thinks India’s speed limit (potential growth) is 6–6.5%. With an investment ratio of 33.8%, if capital is used even moderately efficiently, the speed limit moves to 6.5–7.0%. This means India can grow faster without triggering inflation.

- Quality Control: Most of this is going into transport and urban assets—things that boost productivity. If this were just building “bridges to nowhere,” I’d be worried. But it’s not.

India has quietly shifted to a higher-investment equilibrium. This raises the ceiling for the medium term.

6. How to read the external sector: 6.4% export growth vs 14.4% import growth?

Data recap (real terms):

- Exports: +6.4%.

- Imports: +14.4%.

The bears see a trade deficit and panic. I see a “Capex Deficit,” which is totally different. Double-digit import growth tells you domestic demand is roaring. Single-digit export growth tells you the world is slow. India is powering its own engine right now.

- The “Good” Imports: What are we importing? Capital goods, energy, raw materials. You import these things when you are building capacity (see point #2). You import to build factories, not just to buy gold. This is “Healthy Dependence.”

- The Vulnerability: Yes, it tightens the financing need. We need capital inflows to pay for this. But as long as the global environment is benign, this is fine.

India is currently a “Domestic-Demand” story. It provides insulation from global demand shocks, but sensitivity to global price shocks (US Tariffs, Oil(Inran Crisis)).

7. How should we then approach the US tariff and 500% bill risk?

Data recap:

- Existing: ~50% tariffs on some sectors.

- Tail Risk: Proposed “Sanctioning Russia Act” with 500% tariffs.

Markets are probability-weighing machines. They price the likely, not the merely possible.

- The Tail Risk: A 500% tariff is a “low-probability, high-impact” event. It’s a political bluff. If it happens, it would knock 0.5–1.0% off GDP and crush the Rupee. But betting on it now is speculation, not investing.

- The Base Case: The current 50% tariffs are annoying but manageable. They hurt specific exporters (textiles, leather) but don’t derail the macro story.

- The Pivot: This risk just accelerates what India needs to do anyway—buy less Russian oil, sell more to Europe/Africa, and hug the US diplomatically.

Treat this as a stress test, not a forecast. It adds a risk premium, but it shouldn’t scare you out of the market.

8. What does all this imply for India’s potential growth and macro “quality”?

Putting the pieces together: Real GDP at 7.4% with high Capex means the underlying potential is likely near 7%.”. The current “deflationary impulse” is weird, but positive. It proves India can run high growth without hitting an inflation wall immediately.

- The Fault Line: It’s the Urban/Rural divide. The economy is macro-sound but socially brittle.

- Policy Space: The RBI has room to cut (or stay neutral) because inflation is low. The Fisc has to be careful because nominal tax bases are weak.

If you think like a strategist, the FAE message is clear: India is in a rare “Sweet Spot.” We have High Real Growth, Low Inflation, and Strong Investment. The sustainability of this Goldilocks phase hangs on two things:

- Can politics handle the rural income stagnation without blowing the budget?

- Can we navigate the external trade risks (Tariffs/Oil)?

If those two hold, the Capex-Services engine has plenty of runway left.

9. Then the big question is – How to trade this?

The answer is you follow the money trail who funds the boom (the toll collectors- the Financials and Banking). Think about it: you can’t have a capex boom without a credit boom, and that record-high 33.8% investment ratio is funded by debt. While the consensus worries that low inflation will crush bank margins, they are missing the Volume Story—the sheer scale of lending required for highways, factories, and housing more than compensates for tighter spreads. Large-cap private banks and industrial lenders are effectively the “toll collectors” on this 7.4% growth; every time a new project breaks ground, these lenders take a cut, making them the smartest way to play a volume-driven expansion.

The Final Verdict: Don’t Bet Against the “Builder”

If you take one thing away from this FAE print, let it be this: India has changed lanes.

We are no longer just a “consumption story” waiting for the next festival season to spike sales. We are a “capital formation story” building the runway for the next decade.

The skeptics will point to the rural pain and say the growth is “uneven.” They are right—it is uneven. But in investing, unevenness creates alpha. The gap between the booming industrial/services economy and the lagging rural economy is exactly where the opportunity lies.

Bull markets don’t die on skepticism; they die on euphoria. Right now, there is zero euphoria. Everyone is worried about the farm sector, the US tariffs, and the global slowdown. That “Wall of Worry” is the healthiest thing this market has going for it. It means there is plenty of room for positive surprises.

Your Move: Stop chasing the “Old India” (inflation hedges, rural staples) and start backing the “New India” (credit, infrastructure, urban demand). The economy is building capacity at a record pace. Your portfolio should be funding it.

Ignore the noise. Watch the Capex. Stay invested.