For the past 18 months, the boardroom at Britannia Industries—much like its peers at Nestle and Tata Consumer—has been grappling with a singular, frustrating equation: how to grow when the customer refuses to pay more?

The answer, it turns out, wasn’t in marketing or innovation. It was in the deflator.

Post-November 10, the normalisation of “GST 2.0″—consolidating multiple frantic tax slabs into a cleaner 5% and 18% regime—handed FMCG giants a lifeline. But the macroeconomic tailwind was even stronger. The implicit GDP deflator has collapsed to a historic low of 0.6%. This effectively ended the inflationary era, forcing companies to pass on benefits. Britannia didn’t just pocket the difference; they added grammage. They made the pack heavier, the price constant, and waited.

It worked.

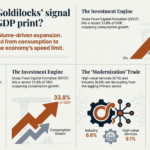

According to the latest Nuvama Consumer Sector Report for Q3FY26, the sector is poised for a “material acceleration” with volume growth estimated at 6%. On the surface, it looks like the start of a new bull run—the “Goldilocks” scenario of benign input costs and policy support.

But scratch the surface of this recovery, and you find a market that is deeply bifurcated and staring down the barrel of a “Nominal Trap.”

The Pivot from Price to Volume: A Forced Hand

For the last two years, FMCG growth was an illusion—”value-led” growth driven by price hikes. Q3FY26 marks the structural break. The Advance Estimates show Real GDP growing at 7.4%, while Nominal GDP is lagging at just 8.0%.

This 60-basis point spread is historic. It signals that the “money illusion” is over. Growth is no longer inflationary; it is purely physical.

Take Tata Consumer Products. While headline revenue growth is projected at 12.5%, the real story is in the tea leaves. Tea volumes are forecast to surge 41% YoY. Why? Because tea prices dropped 8% YoY, and the company kept prices flat to chase volume. This is the “operating leverage” game: covering fixed costs on the first million units so the profit on the next million flows straight to EBITDA.

The Urban “Catch-Up” vs. The Rural “Nominal Trap”

For seven consecutive quarters, the narrative was that “Bharat” (Rural India) would save “India” (Urban India). The new data violently flips this script.

The rural economy is not just “cooling”; it is in a value crisis. While the agricultural sector is producing record volumes (Real GVA +3.1%), the income generated from it is stagnant (Nominal GVA +0.8%). Farmers are harvesting more but earning the same, creating a “volume growth, value stagnation” paradigm.

- Rural: Bumper harvests are meeting crashing prices. With nominal income growth at nearly 0%, rural demand for mass-market FMCG is capped.

- Urban: Conversely, the urban consumer is enjoying a “real income” boost. With CPI collapsing to ~0.7% , the purchasing power of the salaried class has risen, fueling the “catch-up” trade in processed foods and durables.

The “Alpha” bet for H2FY26 is no longer the rural-heavy portfolio. It is the urban turnaround story—companies like Godrej Consumer and Pidilite, where the recovering urban wallet is finally opening up.

The Margin Mirage and the Currency Cliff

If volume is the engine, low input costs are the fuel. Palm oil, tea, and coffee are down significantly YoY. Gross margins for import-heavy majors like Nestle and HUL are expanding by 200-300 basis points.

But there is a skunk at the garden party: The Import Surge.

Real imports are surging at 14.4%, more than double the rate of exports. This has blown out the trade deficit and left the Indian Rupee vulnerable. With the INR trading near historical lows, the “landed cost” of imports is rising—an invisible tax that threatens to wipe out the commodity savings.

- The Exposed: HUL (palm derivatives) and Asian Paints (crude-linked resins) are heavily import-dependent.

- The Safe: Britannia and Tata Consumer source largely within India, insulating them from the currency shock.

The Outlook: Renting the Recovery

The Q3FY26 recovery is real, but it is rented, not owned.

It is built on the shaky foundation of a collapsed deflator and cyclical commodity weakness. The moment inflation returns—or if the Rupee creates a cost-push shock—the “volume party” could end.

For the next six months, the strategy is clear:

- Stick to Domestic Supply Chains: Tata Consumer and Britannia remain the top picks. They have volume momentum and are shielded from the “Import Surge”.

- Avoid the “Nominal Trap”: Be wary of deep-rural plays where income stagnation (0.8% growth) will cap upside.

The Indian consumer is eating again, but only because the menu prices haven’t changed. In a market devoid of pricing power, volume is the only game in town.