I turned on the financial news this morning and nearly spilled my coffee.

Then I opened X—and the signal-to-noise ratio collapsed entirely.

The narrative is everywhere. Loud. Confident. Unquestioned. And in my view, dead wrong.

The headline story goes something like this: “Venezuela is back.” Maduro is supposedly out, Washington is suddenly cooperative, and the oil majors are warming up for a throwback tour—party like it’s 1999. The bulls are rushing into U.S. supermajors—Chevron, ExxonMobil, and maybe even ConocoPhillips—betting that American capital will sweep back into Caracas, unlock the world’s largest proven oil reserves, and print shareholder returns on demand.

This is classic irrational exuberance—the kind that substitutes a compelling geopolitical narrative for the far less exciting reality of a balance sheet.

Major oil companies don’t drill because they can. They drill because the math works. And right now, the math on Venezuela doesn’t resemble a gold mine. It resembles a capital-destruction machine.

Years of underinvestment, institutional decay, sanctions risk, contract uncertainty, and infrastructure degradation don’t disappear because headlines change. Reserves in the ground are not the same thing as cash flow in the bank. For companies whose capital discipline has been forged by a decade of shareholder punishment, Venezuela is not an obvious opportunity—it is a high-risk, low-control, long-dated wager.

If you’re buying the majors today on the expectation of a Venezuelan windfall, you’re not early.

You’re ignoring reality.

And you’re missing five critical truths that the market seems determined to overlook.

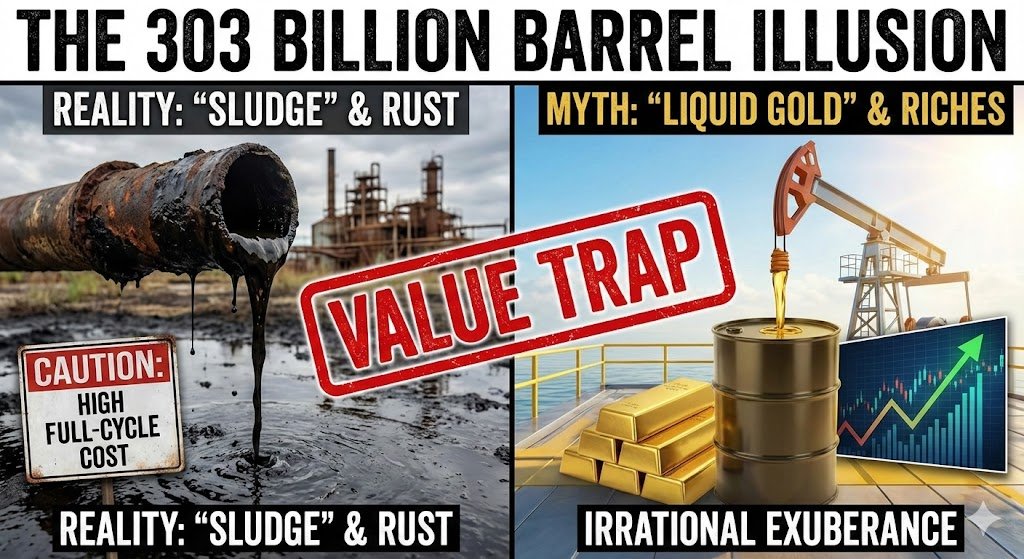

1. The Physics Problem: It’s Not Liquid Gold, It’s “Sludge”

The first mistake the consensus makes is assuming all oil is created equal. It isn’t. In the Permian Basin or Saudi Arabia, you poke a hole in the ground and light, champagne-like crude bursts out, ready to be refined.

Venezuela is a different beast entirely. Its 303 billion barrels are overwhelmingly “extra-heavy” crude from the Orinoco Belt. We aren’t talking about regular oil here. We are talking about “thick, sulphurous sludge” with an API gravity of 8-16 degrees. For the non-geologists: bitumen is denser than water. In the reservoir, it’s hot enough to move. Once it hits the surface temperature, it turns into molasses.

To move this material one inch through a pipeline, you have to mix it with roughly 30-40% “diluent”—expensive light fuels, such as naphtha or condensate. Under sanctions, Venezuela’s supply chain for diluent collapsed, forcing them to rely on sporadic shipments from Russia and Iran. Those supply lines are now broken. You can’t just “turn on the taps” because the taps are clogged with tar. Without a massive, steady, and expensive river of imported diluent flowing in, no crude flows out.

2. The $8 Billion Rust Bucket

Let’s say the new government hands the keys to Chevron tomorrow. Great. Now, how do you get the oil to a ship?

You don’t. The infrastructure is ruinous. We are talking about pipelines that are 50 years old and leaking “almost daily” due to severe corrosion. An internal PDVSA estimate—leaked before the crash—pegged the cost just to fix the pipelines at $8 billion. That isn’t for new growth; that is just to patch the holes.

Then there are the “Upgraders”—the massive industrial complexes designed to strip the sulfur out of that sludge and turn it into sellable synthetic crude. They are largely scrap metal right now. nearly 500,000 barrels per day of processing capacity is currently offline, having been cannibalized for parts or charred by fires over the last five years.

Fixing this isn’t a “weekend project” for a few engineers. It is a capital project akin to rebuilding a small city. It requires specialised compressors, valves, and pumps that have a 12- to 18-month lead time. The idea that this will be solved by 2026 is a fantasy.

3. The Unit Economics: Why “Cheap” Oil is Actually Expensive

This is the dimension the bulls miss, but it’s the only one a CEO cares about. Why would ExxonMobil or Chevron invest billions in a Venezuelan quagmire when they have high-margin, low-risk barrels being pumped in Guyana or the Permian right now?

We need to distinguish between Lifting Costs and Full-Cycle Costs.

- Lifting Cost: Yes, physically pulling a barrel out of a Venezuelan well is cheap—maybe under $10/bbl.

- Full-Cycle Cost: This is where the trade dies. To sell that barrel, you have to buy the diluent at market rates. You have to build your own power plants because the national grid is dead. You have to repair the port terminals.

- The Hurdle Rate: To justify a mega-project to shareholders, a major needs a 15-20% internal rate of return (IRR). Wood Mackenzie estimates it would take $15-20 billion over a decade just to add 500,000 barrels per day.

For that massive upfront check to clear the hurdle, oil prices need to stay high—likely above $60/bbl—forever. If prices soften (perhaps due to the very supply fears the market is worried about), the margins on these heavy barrels vanish. A disciplined board isn’t going to sanction a 10-year project with razor-thin margins.

4. The “American Savior” Fallacy

Investors seem to think U.S. majors are waiting on the border with engines revving, desperate to get back in. They aren’t. They are practicing Capital Discipline.

Look closely at Chevron’s behavior. They’ve been in Venezuela this whole time under special licenses. But they weren’t drilling for growth; they were drilling for debt recovery. They were lifting oil essentially to pay down the billions PDVSA owed them. That is a liquidation strategy, not a growth strategy.

And the others? ConocoPhillips and Exxon have massive unpaid legal claims—$8.7 billion and $1.6 billion respectively—from when their assets were expropriated a decade ago. They aren’t sending new money into a country that hasn’t paid its old bills. They want cash settlements and legal guarantees, not drilling permits.

5. The Political Quicksand: Why the “Risk Premium” is Lethal

Here is the final nail in the coffin: Political Stability. The market is acting like the removal of Maduro is a “Mission Accomplished” moment. History tells us it’s actually the start of the chaos.

- The “Whipsaw” Risk: We’ve seen this before. Sanctions are lifted, then snapped back. Licenses are granted, then revoked. Do you think a CEO is going to sign a 30-year infrastructure deal when the policy environment changes every six months?

- The Creditor Brawl: It’s not just the U.S. majors. There is a line of creditors holding over $150 billion in claims against Venezuela—from defaulted bondholders to the Chinese government to Canadian miners. They will all be fighting to seize every dollar of oil revenue that flows out of the country. This creates a legal minefield where assets can be frozen and accounts seized at any moment.

- The Security Void: Even with a new government, the risk of sabotage, insurgency, or “chaos and constraint” remains high. Pipelines are easy targets.

Markets hate uncertainty. And right now, Venezuela is the definition of uncertainty. To invest here, a company would demand a massive “Risk Premium,” which destroys the already fragile unit economics I mentioned in Point #3.

The Bottom Line

Markets love a good “reopening” story, but they often misprice the cost of the cleanup. The consensus view is that Venezuela is a lottery ticket for the producers. My view is that it’s a value trap.

- The Trap: Don’t buy the majors expecting a Venezuelan windfall. The unit economics simply don’t support an aggressive expansion, and the political risk is toxic to capital.

- The Real Trade: If you want to play this, look at the U.S. Gulf Coast Refiners (like Valero or PBF). They are the ones who actually benefit immediately. They get to buy the discounted heavy crude to feed their specialized coking units, without having to spend the billions to dig it out of the ground or worry about who is running the presidential palace in Caracas.

My Take: The oil is there. The profit isn’t. Until the rust is cleared, the lawsuits are settled, and the politics stabilize, fade the producers and stick to the refiners.